New York and Co (NWY) hit its 52 week low on Tuesday 05/16/17. This coupled with an oversold multiyear price decline and stable fundamentals creates a unsustainable market discount. Further, the market is pricing NWY as if its ultimate future matches recent bankrupt peers; Aeropostale, Limited Stores, PACIFIC SUNWEAR, Wet Seal, and others. This post started as an effort to find mispriced survivors within a devastated industry.

New York and Co (NWY) is a specialty retailer of women's apparel and accessories. Headquartered in New York and founded in 1918. It's a modern wear to-work women's retailer offering feminine fashion, trending and versatile styles. The target customers are women between the ages of 25 and 45. Lastly, as of January 2017 NWY operated 466 stores in 39 states along with an online presence nyandcompany.com.

Investment thesis is simple. The current valuation underestimates years of steady although not exceptional financial results. Years of consistent top line revenue supported by dependable positive CFFO, EBITDA, and improving gross margins. NMY's conservative financial management is evident by years of positive M Scores, Sloan Ratios, and Z Scores. To summarize, market ignores years of reasonable and stable financial performance coupled with opportunities for improved operational execution.

Bottom line for the bears, quarter after quarter NWY reports negative net income. However, this negative does not justify the current stock price. The most conservative EPV (Earnings Power Value) calculation supports a higher stock price. Adjust expenses down for future growth captured within SGA, DDA (Depreciation Depletion Amortization), capital expenditures, new leases, and related taxes. Use the reduced expense calculation coupled with estimated revenues. Then total with the cash balance of 88M less LTD. This aggregate calculation is positive and after applying a conservative market multiple the calculation supports a higher price. Additionally, look at the current 20.20M enterprise value. Now compare to TTM revenue of 929.08M, gross profit 263.98, EBITDA 7.42M or the 20.71M average from 2012 to 2016.

Okay, the challenges are real with no moat, no growth, and within a permanently depressed industry. Yet, NWY has operational opportunities to add on with their years of sound financial management.

Operational positives were discussed during the May 18th Q1 2017 conference call. They covered eCommerce,gross margins,inventory,real estate, celebrity collaboration and sub brands performance.

Gross margins continue to improve. In fact, Q1 2017 GM% reached its highest level since Q1 2008. Ecommerce reported strong double digit increase in sales. Management commented during the Q1 2017 conference call. "strength of eCommerce in Q1 was amazing and was driven by improved conversion, increased traffic and strong product acceptance along with our continued focus as an omni-channel business." Ecommerce business grew from $88 million during 2013 to $226 million in 2016. Inventory, management extends improved execution with an 8% decline for on hand inventory per store.Real Estate, management negotiates rent reductions and flexible terms. Over 60% of leases are on two-year renewals. NWY plans to open 6 to 10 stores in premier locations at attractive rents with low capital investments. During the first quarter the Company opened five New York and Company stores,one outlet store and refreshed three stores. Eight NWY stores closed and one outlet. Unique apparel offerings with celebrity collaboration and sub brands. These performed above expectations and is expanding.

Historical Comparisons aggregated into three buckets, Avg 2012 to 2016, 2015, Current/TTM.

Current Valuation offers reasonable fundamentals. Enterprise value per share calculation (see below) is $0.3155. This compares favorably to the gross profit annual average per share since 2013 to the MRQ of 4.11. Annual revenue per share since 2013 to the MRQ is 14.96, CFFO per share annual average since 2013 to MRQ is .43. The year ending 2014 enterprise per share was 3.42 per share versus today's value of .3155 (90% drop in value). Share count is stable with 63.24M as of 2014 versus today's count of 64.20M

Enterprise Value Calculation = MC 96.66 - Cash (88.37M) + LTD and Capital Lease Obligation (11.485m) +Current Portion (.841M) = 20.25M or EV Per share = .3155

Apparel Store Comparison

Comments: NWY is at or near the worst stock performing stock against 26 peers for 12 months and 3-year time periods. Furthermore, lowest valuation for EV/Sales. Ranked 22 out of 26 for the largest annual revenue with TTM revenue of 929.081. Enterprise is near lowest at 22M coupled with the lowest short ratio (1.60%) and institutional ownership (35.19%).

Negatives:

Apparel Stores continue to rack up bankruptcies. The declining mall traffic, expensive leases, payroll costs , and growing competition from online shopping.

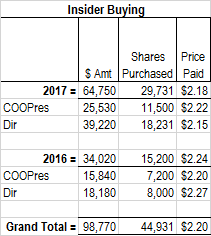

NWY large inside ownership makes acquisition less likely.

No moat with a heavy payroll burden.

In conclusion, my long position is rationalized with "there are no bad assets just bad prices".

Long NWY